Here we are again, at the peak of the boom portion of the economic cycle. How is this time around similar to, or different from previous boom peaks? By looking at various factors that influence economic activity in Canada since the nineteen seventies, we can see some important changes locally and globally.

Economic cycles take approximately 15 years from peak to peak, or trough to trough. Therefore, for approximately 7 to 8 years we experience an increase in economic activity followed by a slow down which also lasts approximately 7 to 8 years. The previous peak occurred in the early nineties, around 1992/93, followed by a down turn that bottomed out in around 1999/00. The previous trough was in 1984/85.

This cyclicality can be seen when looking at various indicators. The latest Statistics Canada employment and building permit numbers verify that nationally, economic activity in 2008, to date, was slower than in 2007. The unemployment rate for January to June 2008 was higher and building permit totals were lower. However, there is considerable internal variation within the country. For example, the proportion of buildings for industrial facilities remains high in Alberta (over 30%) and New Brunswick (over 20%), both well above the national average (~7%). British Columbia has opted for less industry with only 2% to 3 % of building permits for industrial facilities, by far the lowest proportion in Canada. The largest spending on industrial facilities in Canada continues to be in Ontario, but this has declined from over fifty percent of Canadas industrial building, to approximately one third followed closely by Alberta.

Why is industrial activity important to consider when discussing boom and bust cycles? Boom and bust cycles are steeper in areas dependant on raw resource exports with little secondary or tertiary refinement. When raw resource supply is high and demand is low, there will be fewer jobs, less income, less in-migration and more out-migration. People living in areas with the capacity to refine raw resources gain employment and improved wages and benefits when low input costs fuel industry and manufacturing.

However, in BC the next downturn will likely be at least as steep as that of the late 1990s, since wood processing has suffered from the tariff imposed by the USA and as has ship-building with the dismantling of the facilities in North Vancouver and reduction in other refinement activities.

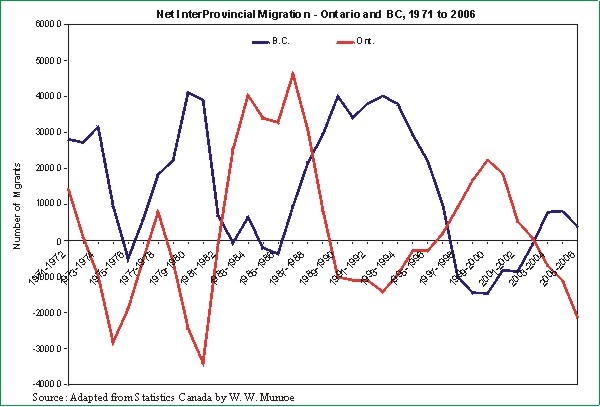

Another indicator of variation in economic activity is migration. Migration tends to lag changes in economic activity, as people do not move as soon as the economy slows.

The last boom time in the early 1990s saw an increase in net migration (in minus out) to the province of approximately 40,000 people per year from 1990 to 1994 before becoming negative in 1998. This time around, net migration to BC peaked at around 10,000.

While BC has the largest port in Canada, providing many opportunities in the core area of the Greater Vancouver Regional District, (GVRD) the rest of the province is vulnerable to a dependancy on raw and primary resources.

The preference for less industry and more tourism and retirement is an orientation and expression which will result in many young adults continuing to move to Alberta while BC attracts more retirees.